SpaceX's $60B Cursor acquisition: deal terms, dilution math, and what it means for shareholders

Inside the all-stock transaction announced June 16, 2026

著者: Compound Team · 2026年7月14日 · 8分で読む

Executive summary

SpaceX (SPCX) announced the acquisition of Anysphere, Inc. (d/b/a Cursor) for $60B in an all-stock transaction on June 16, 2026 — just four days after SpaceX’s Nasdaq IPO at $135/share. The deal values Cursor at 15x LTM ARR ($4B) and 10x projected 2026E ARR ($6B). The floating exchange ratio, based on a 7-day VWAP of SPCX before close, creates meaningful dilution sensitivity: SPCX has declined 38% from its ATH of $225.64 to $139.01 today, increasing implied dilution from 2.0% to 3.2%. We view the strategic logic as compelling — Cursor gives xAI/Grok an immediate enterprise distribution channel with 50,000+ clients and 60%+ Fortune 500 penetration — but the deal’s economics are deteriorating daily as SPCX stock weakens.

Deal snapshot

| Term | Detail |

|---|---|

| Transaction value | $60.0B |

| Consideration | 100% SPCX Class A stock |

| Exchange mechanism | Floating (7-day VWAP before close) |

| Announcement date | June 16, 2026 |

| Expected close | Q3 2026 (pending regulatory) |

| Target LTM ARR | $4.0B (300%+ YoY growth) |

| Implied multiple (LTM ARR) | 15.0x |

| Implied multiple (2026E ARR) | 10.0x |

| Dilution at announcement ($226) | 2.0% |

| Dilution at current ($139) | 3.2% |

| Premium to Series D ($29.3B) | 105% |

| Breakup fee | $1.5B cash + $8.5B compute |

Acquirer: SpaceX (SPCX)

SpaceX completed its Nasdaq IPO on June 12, 2026 at $135/share, raising $75B and achieving a $1.77T market cap1 — making it the largest IPO in history. The company operates across three segments: Connectivity (Starlink, $11.4B revenue, 62.9% EBITDA margin), Space (Falcon 9/Starship, $4.1B), and AI (xAI/Grok/X, $3.2B, operating at -$6.4B loss). Total FY2025 revenue was $18.7B with $6.6B adjusted EBITDA and a $(4.9B) net loss driven by heavy AI infrastructure investment. Starlink subscribers grew from 2M (end 2023) to 10M (Q1 2026). At IPO pricing, SPCX traded at 94.6x EV/Revenue and 268x EV/EBITDA2 — reflecting the market’s valuation of SpaceX’s monopolistic position in reusable launch and global satellite connectivity.

| Segment | Revenue | Operating income | EBITDA | Margin |

|---|---|---|---|---|

| Connectivity (Starlink) | $11.4B | $4.4B | $7.2B | 62.9% |

| Space (Falcon 9 / Starship) | $4.1B | Profitable | — | — |

| AI (xAI / Grok / X) | $3.2B | $(6.4B) | — | — |

| Total | $18.7B | — | $6.6B | 35.3% |

Target: Anysphere (Cursor)

Cursor is the fastest-scaling B2B SaaS company in history — founded in 2022 by four MIT students (M. Truell, S. Asif, A. Sanger, A. Lunnemark), the AI-native code editor reached $4B ARR by June 2026, up from $100M in January 20253 (a 40x increase in 18 months). Enterprise revenue accounts for 65% of total ($2.6B), with 50,000+ enterprise clients and 60%+ Fortune 500 penetration. Cursor generates 150M+ lines of enterprise code daily and holds 26% market share in the $9.5B AI coding tools market4. The company raised ~$3.4B across six rounds, with its Series D in November 2025 at a $29.3B valuation (led by Accel and Coatue). The $60B acquisition price represents a 105% premium to the Series D and 20% above a planned $50B round.

| Period | ARR | Growth (from prior) |

|---|---|---|

| January 2025 | $100M | Baseline |

| June 2025 | $500M | +400% |

| November 2025 | $1,000M | +100% |

| December 2025 | $1,200M | +20% |

| February 2026 | $2,000M | +67% |

| June 2026 (at acquisition) | $4,000M | +100% |

| Round | Date | Amount | Valuation | Lead investor(s) |

|---|---|---|---|---|

| Seed | 2023 | $8M | N/A | OpenAI Startup Fund |

| Series A | Aug 2024 | $60M | $0.4B | Thrive Capital |

| Series B | Jan 2025 | $100M | $2.6B | Thrive, a16z |

| Series C | May 2025 | $900M | $9.9B | Thrive, Accel, a16z, DST |

| Series D | Nov 2025 | $2,300M | $29.3B | Accel, Coatue |

| Total | — | $3,368M | — | — |

Valuation & deal structure

The transaction is structured as 100% SpaceX Class A stock with a floating exchange ratio based on the 7-day VWAP of SPCX preceding close. There is no price collar or walk-away trigger disclosed — SpaceX is committed to delivering $60B regardless of stock price5. The breakup fee (if the option is not exercised) is $1.5B cash plus $8.5B in computing resources. Microsoft considered but declined to bid; OpenAI made two separate approaches that were turned down.

| Sources | Amount | % | Uses | Amount | % |

|---|---|---|---|---|---|

| SPCX Class A stock | $60.0B | 100.0% | Equity to Anysphere | $60.0B | 99.7% |

| Cash | $0.0B | 0.0% | Transaction fees | $0.2B | 0.3% |

| Total sources | $60.0B | 100.0% | Total uses | $60.2B | 100.0% |

At 15x LTM ARR, the deal appears reasonable relative to Cursor’s growth trajectory (300%+ YoY) — the Wiz/Google deal in 2024 was valued at 46x revenue, and high-growth SaaS (>100% growth) historically trades at ~20x. On a forward basis, the deal is even cheaper: 10x projected 2026E ARR ($6B) and 7.5x estimated NTM revenue ($8B)6.

| Transaction | EV/Revenue | Context |

|---|---|---|

| Cursor (this deal, LTM ARR) | 15.0x | Fastest-growing B2B SaaS ever; 300%+ growth |

| High-growth SaaS (>100% growth) | ~20x | Historical median for triple-digit growers |

| GitHub Copilot (implied) | ~15x | Estimated from MSFT segment reporting |

| Wiz / Google (2024) | 46x | $32B deal at ~$700M ARR |

Pro forma combined entity

The combined entity generates $22.7B in pro forma revenue7, with Cursor contributing 17.6% of the total. The deal transforms SpaceX’s revenue composition — AI-related revenue (xAI + Cursor) rises to 31.7% of the combined entity from 17.1% standalone. At the announcement price ($225.64), the pro forma market cap is $3.0T; at the current price ($139.01), it is $1.9T. Dilution to existing SpaceX shareholders is limited (2.0-3.2% depending on price) given SpaceX’s massive market cap. Revenue per employee diverges dramatically: Cursor at ~$13M vs. SpaceX at ~$849K.

| Segment | Revenue | % of combined |

|---|---|---|

| Connectivity (Starlink) | $11.4B | 50.2% |

| Space (Falcon 9 / Starship) | $4.1B | 18.0% |

| AI (xAI / Grok / X) | $3.2B | 14.1% |

| AI Coding (Cursor) | $4.0B | 17.6% |

| Total | $22.7B | 100.0% |

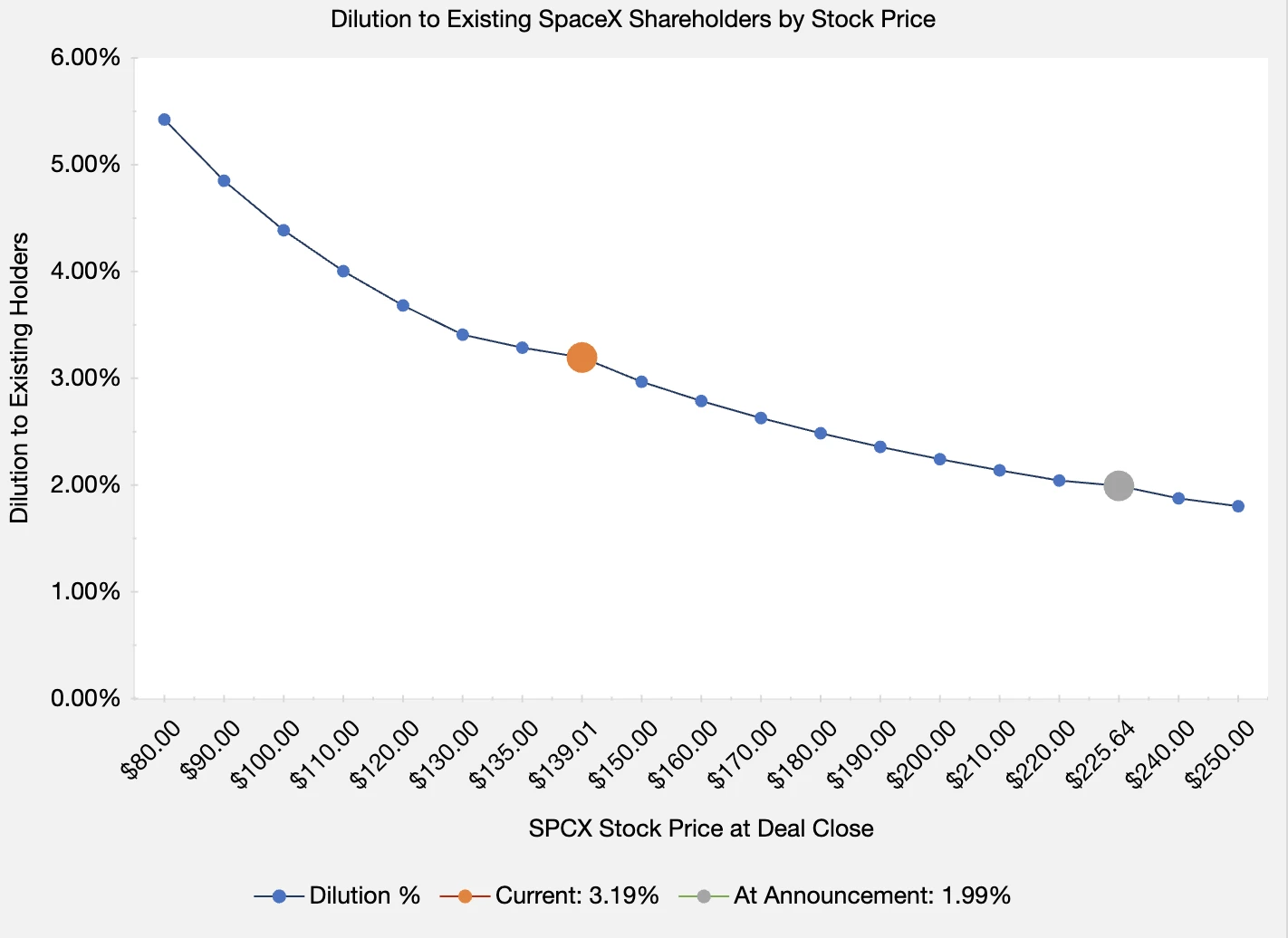

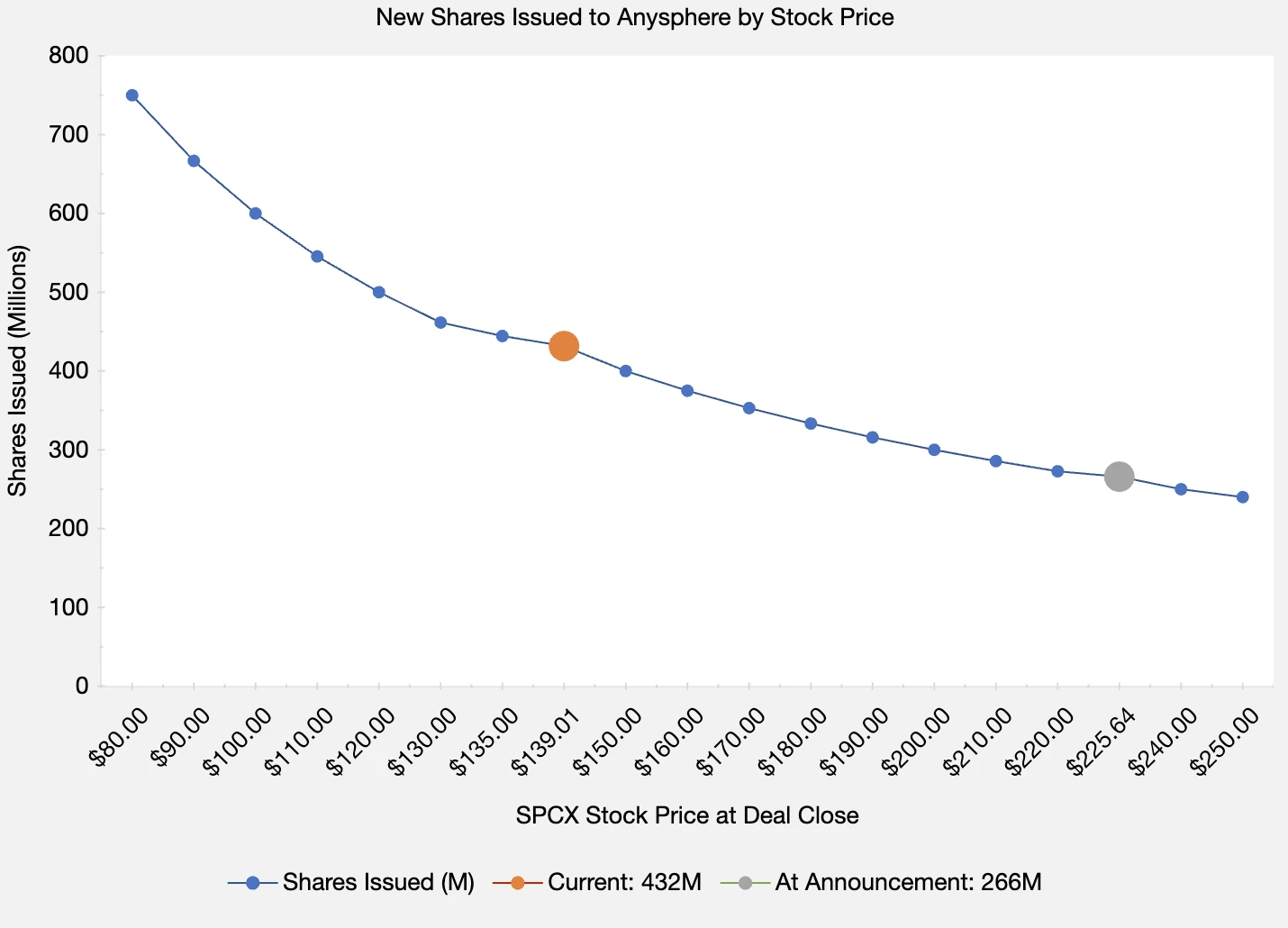

Stock price impact & dilution sensitivity

SPCX has declined 38.4% from its intraday ATH of $225.64 (June 16, the day of deal announcement) to $139.01 today. Because the exchange ratio floats — Anysphere receives $60B in stock regardless of price — the number of new shares issued increases as the stock falls, compounding dilution for existing holders. At the announcement price, SpaceX issues 266M shares (2.0% dilution); at today’s $139, it must issue 432M shares (3.2% dilution)8. If SPCX falls to $100, dilution reaches 4.4% (600M shares). There is no collar or walk-away — SpaceX shareholders bear the full ratchet risk.

| Scenario | SPCX price | Shares issued | Pro forma shares | Dilution % | Addl. dilution vs. ATH |

|---|---|---|---|---|---|

| At all-time high (Jun 16) | $225.64 | 266M | 13,346M | 1.99% | Baseline |

| At deal announcement close | $201.80 | 297M | 13,377M | 2.22% | +0.23% |

| At first day close | $160.95 | 373M | 13,453M | 2.77% | +0.78% |

| At current price | $139.01 | 432M | 13,512M | 3.19% | +1.20% |

| At IPO price | $135.00 | 444M | 13,524M | 3.29% | +1.29% |

| If falls to $120 | $120.00 | 500M | 13,580M | 3.68% | +1.69% |

| If falls to $100 | $100.00 | 600M | 13,680M | 4.39% | +2.39% |

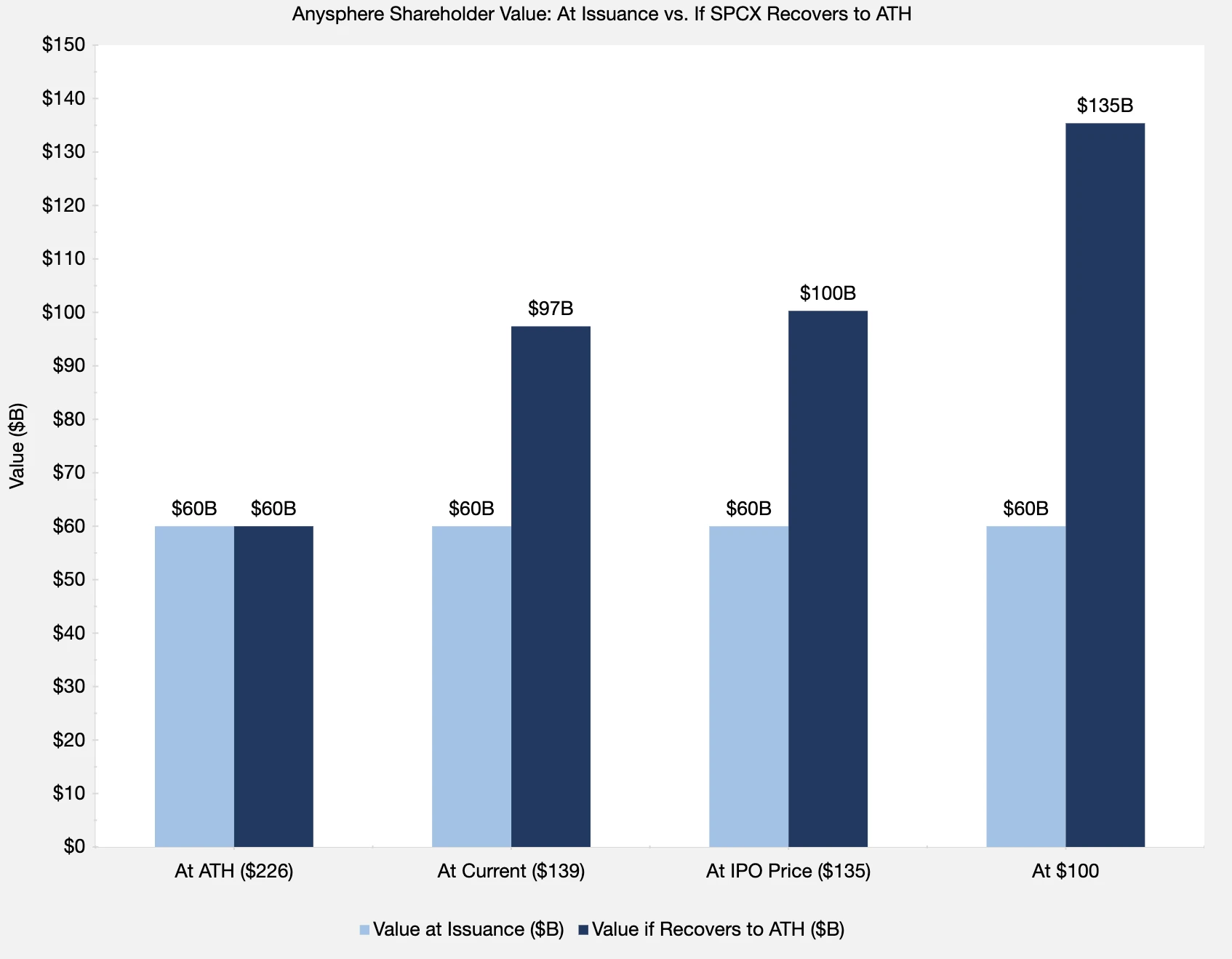

Critically, the asymmetry favors Anysphere shareholders: at lower SPCX prices, they receive more shares, creating embedded optionality if the stock recovers. At the current $139 price, Anysphere receives 432M shares worth $60B today — but worth $97.4B (+62%) if SPCX returns to its ATH9. At $100, they would receive 600M shares worth $135B if SPCX recovers to ATH (a 126% return on $60B cost). SpaceX shareholders face the inverse: declining stock + increasing dilution.

Strategic rationale & investment implications

-

Enterprise AI distribution: Cursor gives SpaceX/xAI immediate access to 50,000+ enterprise clients, 60%+ Fortune 500 penetration, and $2.6B in enterprise ARR. This is the fastest path to monetizing xAI/Grok in the enterprise — a market where SpaceX currently generates losses.

-

Competitive positioning: The deal positions SpaceX directly against Microsoft (GitHub Copilot), Anthropic (Claude Code), and Google (Gemini Code Assist) in the $9.5B AI coding tools market. Combined with xAI’s Colossus supercomputer, Cursor gains a compute advantage its competitors cannot match.

-

Revenue diversification: Cursor adds high-growth (300%+), high-margin SaaS revenue to offset the AI segment’s $(6.4B) operating loss. Pro forma AI-related revenue (xAI + Cursor) is $7.2B — 31.7% of the combined entity.

-

IPO currency arbitrage: SpaceX used its $2T+ post-IPO valuation as acquisition currency within 4 days of listing. At 2% dilution, this is an exceptionally efficient use of stock — typical large-cap tech acquisitions dilute 5-15%. The option was secured in April 2026, suggesting Musk planned this sequence.

-

Key risk — falling stock price: The floating exchange ratio with no collar means every 10% decline in SPCX adds ~25-40 basis points of dilution (accelerating at lower prices). From ATH to current, existing shareholders have already absorbed 120bps of additional dilution10. If SPCX declines further into the Q3 close, economics deteriorate further.

Conclusion

The SpaceX/Cursor deal is strategically logical but structurally aggressive. Acquiring the fastest-growing SaaS company in history at 15x ARR — using stock from a 4-day-old IPO with no downside protection — is a high-conviction bet that SpaceX’s stock will stabilize or recover before the Q3 close. At $139/share (38% below ATH), the deal’s dilutive cost has already increased 60% from announcement levels. We view Cursor’s fundamentals as exceptional ($4B ARR, 300%+ growth, 65% enterprise, 60%+ F500), and the 15x multiple as reasonable given comparables. However, SPCX shareholders should monitor the stock closely — the absence of a collar means dilution is uncapped on the downside.

Sources

All quantitative data, financial figures, and deal terms cited in this report are sourced from the SpaceX - Cursor Acquisition Model (Excel workbook), which contains the following analytical sheets:

- Transaction Summary — deal terms, context, and target background

- Acquirer - SpaceX — company profile, segment financials, IPO data, and valuation multiples

- Target - Cursor — ARR trajectory, revenue mix, market position, and funding history

- Valuation & Deal Analysis — sources & uses, implied multiples, comparable transactions, and dilution analysis

- Pro Forma Analysis — combined entity revenue, segment mix, and strategic rationale

- Stock Price Impact — price timeline, dilution sensitivity scenarios, and Anysphere shareholder value analysis

References

- ‘Acquirer - SpaceX’ sheet, cells B15-B19

- ‘Acquirer - SpaceX’ sheet, cells B44-B45

- ‘Target - Cursor’ sheet, cells B17-B22

- ‘Target - Cursor’ sheet, cells B33-B34

- ‘Transaction Summary’ sheet, cells C11-C14

- ‘Valuation & Deal Analysis’ sheet, cells B22-B24

- ‘Pro Forma Analysis’ sheet, cell D6

- ‘Stock Price Impact’ sheet, cells C30 & E30

- ‘Stock Price Impact’ sheet, cells D58 & E58

- ‘Stock Price Impact’ sheet, cell G30